Bank of India (BOI), one of India’s largest and most established public sector banks, has played a pivotal role in shaping the country’s banking sector since its founding in 1906.

As a prominent financial institution, BOI has built a strong brand and a broad network, positioning it as a significant player within the banking industry.

In this article, we dive deep into the (Strengths, Weaknesses, Opportunities, and Threats) or SWOT analysis of Bank of India, examining its core attributes and exploring the factors that may impact its future.

In this blog

Overview of Bank of India

![]()

Bank of India was founded in 1906 by a group of eminent businessmen in Mumbai, Maharashtra. Since nationalization in 1969, BOI has grown rapidly and now offers a broad spectrum of services, including corporate banking, retail banking, and investment management. BOI’s extensive network includes over 5,000 branches and ATMs across India and several offices overseas.

Quick Stats About Bank of India

| Attribute | Details |

|---|---|

| Founder | Indian Government |

| Year Founded | 1906 |

| Headquarters | Mumbai, Maharashtra, India |

| Number of Employees | 50,000+ |

| CEO | Atanu Kumar Das |

| Company Type | Public |

| Market Cap | $6 Billion |

| Annual Revenue | $5 Billion |

| Net Profit | $300 Million |

Recent Developments in Bank of India

- Digital Transformation Initiatives: BOI has focused on enhancing its digital offerings to compete with private banks and meet customer demands for online banking.

- Government Reforms and Support: Recent governmental support and reforms in the public sector have provided BOI with resources to improve its operational efficiency.

- Partnerships with Fintech Firms: BOI has partnered with fintech companies to provide new digital solutions and innovative financial products for its customer base.

- Environmental and Social Responsibility: BOI has increased its involvement in sustainable financing and renewable energy projects to support environmental causes and align with global ESG standards.

SWOT Analysis of Bank of India

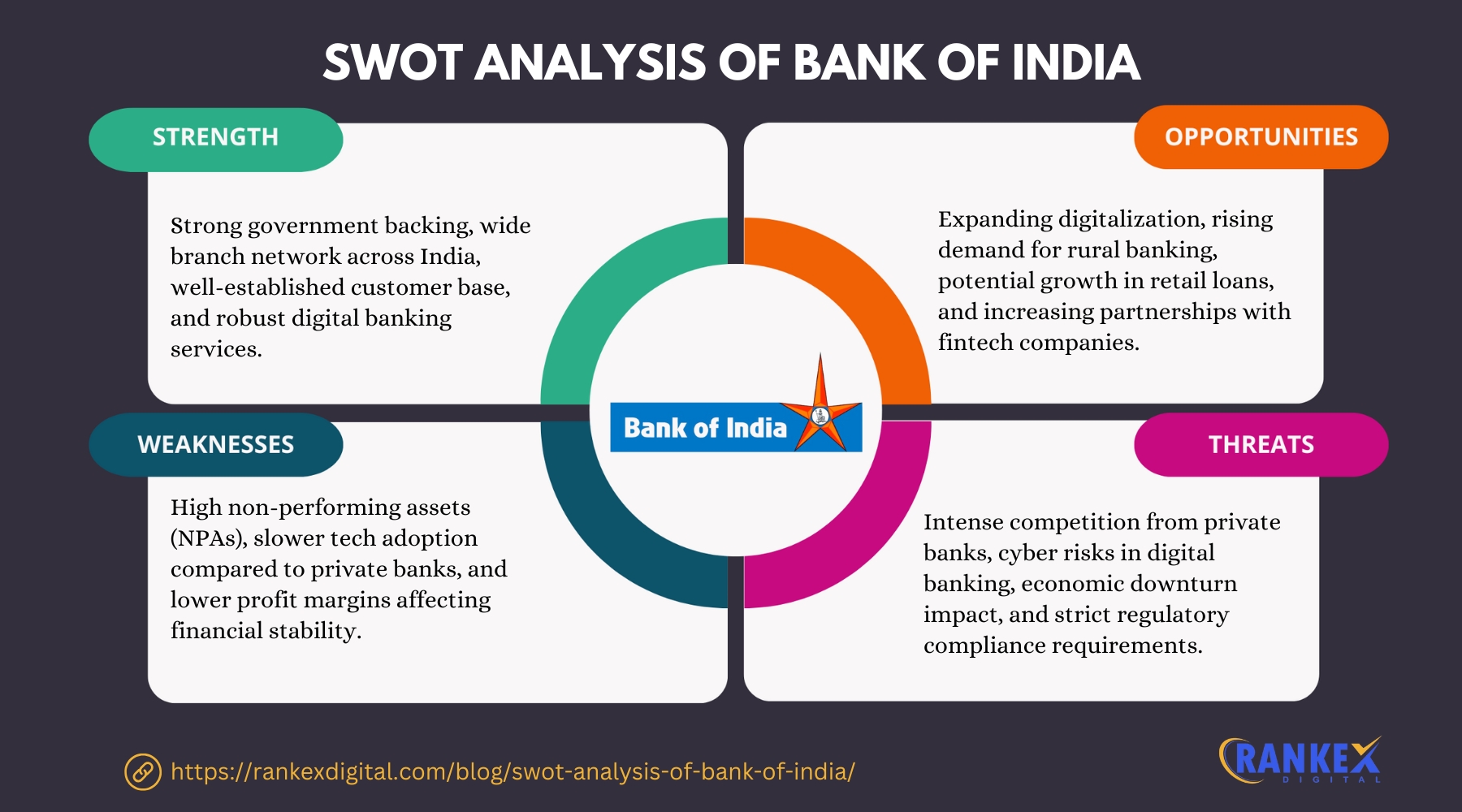

Strengths of Bank of India

- Extensive Network and Reach: BOI has one of the largest branch networks across India, reaching both urban and rural customers. This wide presence promotes financial inclusion, especially in underserved regions, and ensures accessibility to a broad population.

- Strong Government Backing: As a government-owned bank, BOI benefits from the stability and security associated with government support. This backing reassures customers, particularly in times of financial uncertainty, and can provide assistance in accessing funding or support during economic challenges.

- Diverse Service Portfolio: BOI offers a variety of financial products, from personal and corporate banking to international services. This diversification enables BOI to address the needs of a broad customer base, serving different sectors and creating multiple revenue streams.

- Stable Customer Base: BOI has built a loyal and stable customer base over time. This loyalty reduces customer turnover and fosters stable income through repeat transactions and long-term banking relationships, which are key advantages in a highly competitive sector.

- International Presence: With branches in 18 countries, BOI has established a global footprint, especially benefiting Non-Resident Indians (NRIs). This global presence allows BOI to diversify its revenue sources and expand services for customers with international banking needs.

Weaknesses of Bank of India

- High Non-Performing Assets (NPAs): Like many other public sector banks, BOI faces challenges with NPAs—loans where repayment is overdue or unlikely. High NPAs impact the bank’s profitability, drain resources, and necessitate additional provisions that reduce overall financial health.

- Operational Inefficiencies: BOI’s extensive branch network and large workforce can lead to operational inefficiencies, including increased costs and logistical challenges in maintaining effective services across all branches.

- Bureaucratic Processes: As a public sector bank, BOI sometimes faces bureaucratic hurdles that can slow decision-making. This slower pace may affect its ability to compete with private sector banks that tend to be more agile and responsive to changes in the banking landscape.

- Limited Technological Innovation: While BOI has made strides in adopting technology, it often lags behind private sector banks, which are generally quicker to implement cutting-edge digital solutions. This gap in technological infrastructure could affect BOI’s appeal to tech-savvy customers.

- Dependence on Interest Income: BOI’s revenue relies heavily on interest income from loans. This dependence makes it vulnerable to shifts in interest rates and monetary policies, affecting profitability, especially during periods of low interest rates or economic downturns.

Opportunities for Bank of India

- Digital Banking Growth: The rapid growth of digital banking presents an opportunity for BOI to modernize its offerings and appeal to tech-oriented customers. By expanding its digital services, BOI can increase customer engagement and tap into the growing market of online banking.

- Expansion in Rural Areas: India’s large rural population remains underserved by financial services. BOI has the chance to capitalize on its extensive branch network to reach these rural areas, boosting financial inclusion and gaining new customers.

- Diversification of Services: As customer needs evolve, BOI can introduce additional offerings like wealth management and digital payments. Diversifying its services can strengthen BOI’s position by addressing a wider range of financial needs and increasing customer loyalty.

- Strategic Collaborations: Partnerships with fintech companies could enhance BOI’s technological capabilities, allowing it to offer innovative products. Collaborating with fintechs can help BOI deliver better digital solutions and attract younger, tech-savvy customers.

- Global Expansion: BOI has potential to grow its international presence, particularly by serving the financial needs of NRIs. Expanding globally could not only strengthen BOI’s revenue base but also insulate it from domestic market fluctuations.

Threats to Bank of India

- Intense Competition: The Indian banking sector is competitive, with numerous public and private banks vying for market share. This competition requires BOI to continuously innovate and improve to retain and grow its customer base.

- Economic Downturns: Economic slowdowns can increase loan defaults, particularly for public sector banks like BOI with a significant customer base in rural and economically vulnerable areas. Defaults impact profitability and require additional resources to manage.

- Regulatory Changes: Changes in banking regulations, such as stricter capital requirements or lending norms, can directly impact BOI’s operations and financial health. Compliance with new regulations may necessitate additional resources and adjustments in business strategies.

- Cybersecurity Risks: As BOI expands its digital services, it also faces increased cybersecurity risks. A breach or data compromise could damage customer trust, lead to financial losses, and expose BOI to regulatory penalties.

- Global Economic Fluctuations: With branches in several countries, BOI is also exposed to economic changes internationally. Global downturns, currency fluctuations, or political instabilities in foreign markets could negatively affect BOI’s overseas operations and profitability.

Competitors of Bank of India

Conclusion

Bank of India’s SWOT analysis highlights its strong government support, broad branch network, and stable customer base as significant strengths. However, it faces challenges in the form of high NPAs, operational inefficiencies, and bureaucratic processes.

BOI can leverage opportunities in digital banking, rural expansion, and service diversification to strengthen its position in the banking industry. To thrive, BOI must address its weaknesses and proactively manage emerging threats from competition, regulatory changes, and cybersecurity risks.

Frequently Asked Questions

What is the main focus of Bank of India’s digital transformation?

Bank of India is focused on expanding digital services to enhance customer convenience and meet the growing demand for online banking solutions, including mobile and internet banking.

How does Bank of India benefit from government support?

As a public sector bank, BOI receives financial and policy support from the government, which helps in maintaining stability, boosting customer trust, and securing resources for growth.

What are the key weaknesses Bank of India faces?

BOI’s primary weaknesses include high non-performing assets, operational inefficiencies, and slower decision-making processes compared to private sector banks.

How is Bank of India planning to expand in rural areas?

BOI aims to increase financial inclusion by expanding its branch and ATM network in rural regions, offering banking services to underserved populations.

What cybersecurity measures is Bank of India implementing?

To safeguard its digital infrastructure, BOI is investing in robust cybersecurity protocols, including data encryption and multi-factor authentication, to protect customer data and prevent potential cyber threats.